8 steps to create an effective business budget

Statistics from the UK government show that 89% of startups in the UK survive their first year, but only 42.4% of new businesses make it beyond five years.

That begs the question: What’s the difference between businesses that survive and those that fail? A common theme is business budget.

A study of 80+ failed startups indicated that more than 50% of the founders did not have a clear budget for their business when they started.

When you’re building a business from scratch, it’s bound to be financially demanding. You’d likely want to spare no expense in those starting days when you’re getting your business ready for lift-off.

But without a well-designed budget in sight, you can easily get carried away and spend too much money or prematurely assume you’ll make enough revenue post-launch to offset the initial expenses.

In this article, you’ll learn what business budgeting is all about, why it’s important at all stages of your business (but especially pre-launch) and some useful steps to help you build an effective budget for your own business.

Table of contents

- What is a business budget?

- Importance of creating a business budget

- 8 steps to create an effective business budget

- Wrapping up

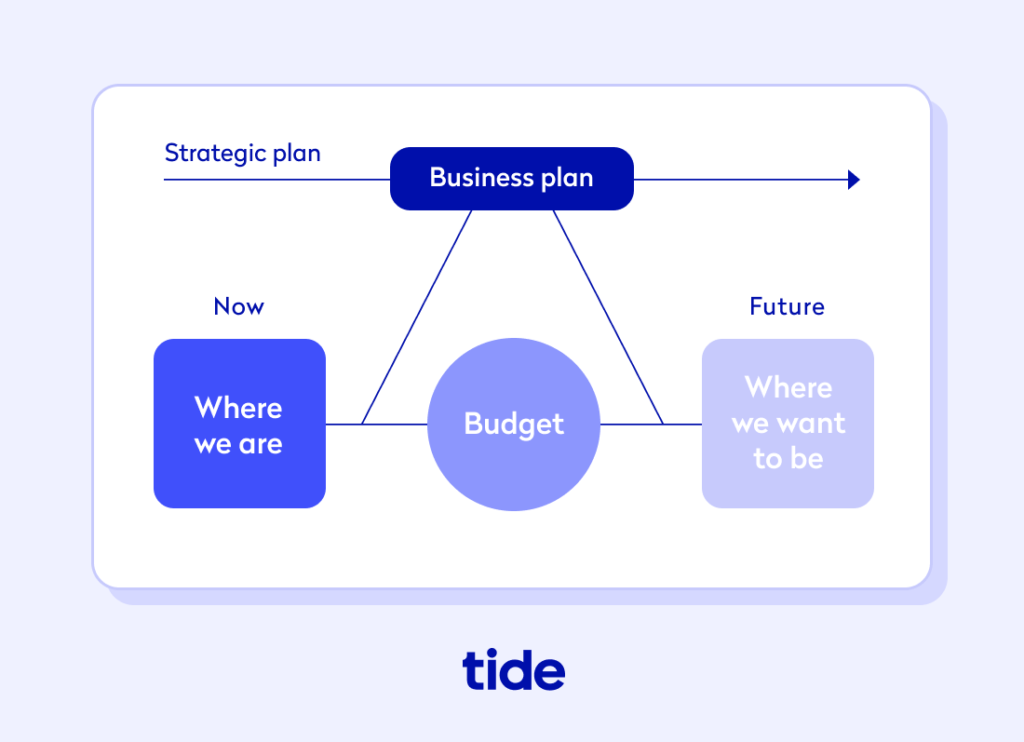

What is a business budget?

A small business budget is a financial plan that provides businesses with key information regarding their capital, revenue and expenditure.

For small business owners, budgets provide an estimation of revenues and expenses over a specified period of time, such as monthly or annually. They also act as a guiding hand to help you determine how and where you’ll spend your money.

The purpose of a budget is threefold:

- Forecast your earnings. Creating a budget helps you estimate the amount of money your business will make in the form of revenue, sales and profit.

- Plan your expenditure. A budget is a way to assign a job to your business spending so that you have a legitimate reason behind every penny you spend.

- Hold yourself accountable. Having a budget lets you evaluate your spending plan vs. spending reality so you can see if you’re actually meeting your desired goals and achieving forecasted expectations.

A small business budget is only as valuable as the amount of frequent and accurate information being recorded in it. It must be compiled and re-evaluated often to ensure it aligns with your business needs and your continually evolving goals.

To improve your business’s chances at success, it’s important that you look at all of your company’s financial information, past, present and future, and create a thorough budget to make sure your total expenses align with your predetermined goals.

Top Tip: No matter where you’re at in your business journey, financial forecasting should be consistently top of mind. Why? Because without an understanding of your projected cash flow, you won’t be able to answer basic questions, such as if and when you can begin hiring talent and if you have the budget to build new products or services. To learn more, read our guide to what a cash flow forecast is and how to create one 🚀

Importance of creating a business budget

If you’re a founder who’s driven to lead your startup to its fullest potential, you need a budget plan in place to ensure your business finances are consistently contributing to your business success.

Business budgets can help you in several ways:

- They stop you from spending money in the wrong places. A business budget helps you to determine if your business costs are essential or optional. Without a budget, you may invest too heavily in optional costs upfront, thus running into trouble down the line if you do not earn enough revenue to remain afloat. A budget provides you with a clear picture of your finances so you can better decide how much money to spend at the right time, in the right way.

- They help you get funding. If you’re hoping to get funding or raise venture capital through banks or investors, know that they will most likely require a detailed business plan that includes a budget so that they can get a clear picture of your forecasted spending. Understanding exactly what their investment will go towards and specifically how it will be spent will help them perform a risk/reward evaluation and make a fully informed decision.

- They set goals for your business. Budgets take into account revenue projections for different timeframes. If you fail to calculate future spending needs, you may not have enough left in your budget to accomplish everything you’ve set out to do. A great business budget will help you to prioritise which goals you can achieve in what order, based on realistic metrics.

- They help identify your problem areas. Your budget plan can help you spot your most draining expenses or costs. The ability to evaluate your actual spending patterns vs. expected spending patterns will help you refocus any missteps and ultimately increase your profit margins and improve your bottom line.

Top Tip: To learn more about how to calculate business startup costs and get a glimpse into 13 common startup costs you may experience as a new business owner, read our guide that explores how much it costs to start a business in the UK 💡

Here are some examples of how you can set goals, strategies, measures and targets in your business budget to hold yourself accountable and ensure you’re spending is aligned with your predefined objectives:

| Goal (What are you trying to achieve? | Strategy (How will you achieve it?) | Measures (What are the inputs and outputs?) | Targets (Quantifiable, time-based) |

| Sell more of X from new product line | Increase marketing and advertising initiatives | Weekly number of inventory sold | Referral deals redeemed, ad traffic acquired |

| Generate £X in new business pipeline | Run virtual events to connect with ideal clients | Monthly and quarterly projected revenue | Number of new leads, sales appointments set |

| Hire X new people in the engineering team | Showcase company culture, hire a headhunter | Successful new hires by internal deadline | New applicants, referrals from network |

8 steps to create an effective business budget

A good business budget is detailed yet flexible. It should act as a living document that you reevaluate and adjust often as your business grows and evolves.

Here are eight steps to help you create an effective budget for your own business.

Top Tip: We’re about to explain some basic accounting practices, and while business accounting is not something you need to master as a small business owner, it is key that you grasp the fundamentals. This will help you to ensure your business remains profitable and help you make informed financial decisions. To learn more, read our complete guide to accounting for startups 📣

Step 1: Estimate monthly fixed costs

When estimating your expenses, it’s helpful to first divide them into fixed and variable costs.

Fixed costs are pretty easy to identify. These are the consistent and recurring expenses that must be paid every month and are necessary to keep the business running.

Fixed costs include things like the rent for your office, insurance expenses, credit card fees and costs of leasing the necessary equipment for your business. Fixed costs can be very high or quite low depending on the nature of your business.

For example, if your business involves manufacturing products, it’s likely to have higher fixed costs related to space and equipment. These costs, however, will be much lower or even non-existent for an online consulting business operating from home.

Calculating your monthly fixed costs is a simple, two-step process.

- From a list of all your expenses, identify the repetitive costs that remain constant each month.

- Add up all these expenses to get the total fixed costs of your business. You can also divide this with the number of units you produce to calculate your fixed cost per unit.

Knowing your fixed costs tells you the bare minimum that your company needs to survive. It’s important to research these expenses and make sure you’re getting the best deal on each cost.

Step 2: Determine variable expenses

Variable costs are, as the name suggests, are costs that vary. They depend entirely on the number of goods or services you need to operate in a given timeframe. Rather than the fixed costs that rarely ever change, such as rent, variable costs change often.

To continue with our manufacturing business example, the variable costs would be the cost of the raw materials and labour that go into producing each unit. The more units you produce, the more input you would require and the higher your variable costs will be.

For service-based businesses, however, it might get a little trickier. For example, if you’re an online business providing content marketing services, how do you associate your variable costs to the services you provide?

First, you choose how you want to quantify your services. Is it in terms of the hours you put into your work or do see your units of service as each individual, completed project?

From there, you can associate the relevant costs to each unit produced, which may be based on the hours spent on the computer, the expenses made on research material, or the cost of using an SEO tool to inform your post’s keyword strength.

At times, it becomes difficult to separate fixed and variable costs in a business. You might consider employee wages to be fixed costs if they’re recurring and must be paid every month. However, this logic does not apply to freelancers or contractors that you hire for specific projects or needs, as their contributions are more sporadic.

Variable costs tend to be more flexible than fixed costs, therefore, if you’re looking to cut costs and increase your profit margins, consider tackling your variable costs first.

Top Tip: To learn more about the different types of expenses and how to manage them, as well as which ones you can claim in order to reduce the amount of income tax you pay as a business, read our guide to what expenses are and how small businesses can manage them 💷

Step 3: Predict one-time costs

Apart from the fixed and variable costs of your business, you must also keep one-time spendings or ‘sunk costs’ in mind and include them in your budget plan. These expenses will be less frequent and more relevant in the initial phase of your start-up.

One-time expenses may include purchasing equipment that you own instead of rent. For example, it could be a computer or certain software you need to carry out your business operations. One-time costs could also include some basic furniture you might need to set up your office or a domain name for your website.

Not all one-off costs can be predicted beforehand, and this is where an emergency fund comes in handy. We will discuss emergency funds in more detail in a later section.

Top Tip: One of the most important one-off expenses is incorporating your business. First, you need to choose your legal business structure. To learn more about each structure in-depth, read our guide on how to register a business in the UK. If you choose to operate as a limited company, you can register your business with Tide for only £9.99! 🎉

Step 4: Project revenues

Once your business starts making money, you need to use your sales activities to forecast future revenue generations. You should be able to estimate the sales you’ll be making in the next week, month and year.

This will provide you and your team with goals you aim to achieve within different timeframes and allow you to accurately compare how well you’re actually doing with how well you expected to do.

The ability to compare/contrast actual revenue vs. projected revenue will help to inform your future projected revenue forecasts. The more that you can align expected vs. projected revenue, the better you can set an intentional budget that helps you to achieve your goals. It also helps you to maintain a healthy cash flow to ensure you maintain consistent financial health.

As a new business, you need to be extra careful with your figures as sales tend to be unpredictable without an established customer base.

Top Tip: To help with accurate predictions before launch, conduct thorough market research to understand how your competitor’s in your target market price similar products or services, if applicable. To learn more, read our guide to how to conduct market research for your business idea 📊

This will help you gauge how much your target audience is willing to spend on similar value propositions. Through market research you can also find, if publicly available, your competitor’s monthly or annual revenue reports to better determine how much revenue you could make in a similar space.

Step 5: Track your profit (or loss)

A good indication of how well your business is doing is your net profit margin, which is the money you’re left with after deducting your operating expenses, interest and taxes.

It’s important to note that profit earned is not the same as revenue generated. Revenue is the money generated through sales before deducting any of the costs. Even if your revenue boasts off an impressive revenue figure, it’s possible that your business is still suffering a serious loss.

You can use our net profit margin calculator to quickly and easily find your profitability in relation to total revenue.

Our net profit margin calculator measures your company's profitability in relation to its total revenue, or in other words how much of each pound received by your business is net profit.

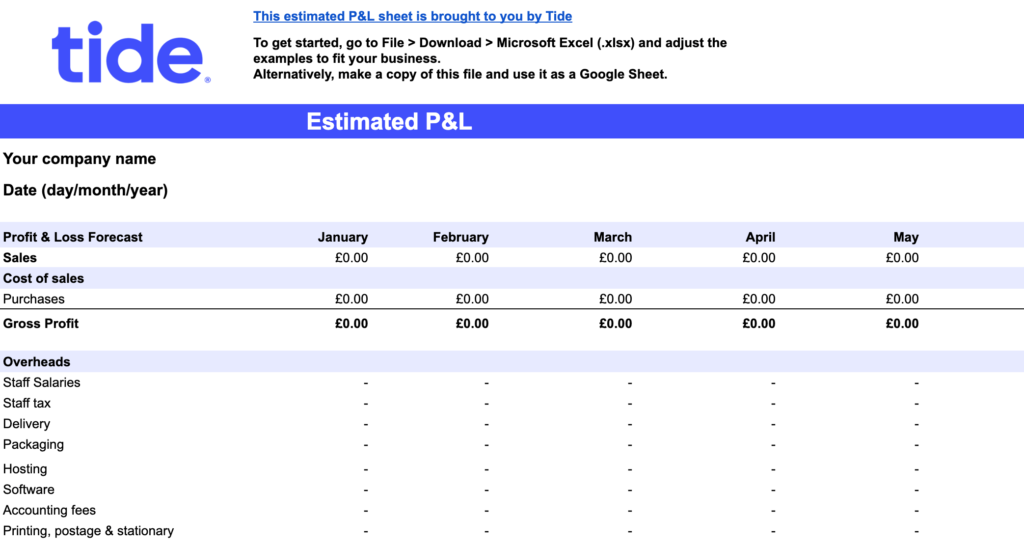

£ £ %It’s also helpful to put together all your financial results into a profit and loss (P&L) statement. With all of your relevant costs already identified and with your revenue figures in hand, you only need to carry out some simple additions and subtractions to create your P&L statement.

Here’s an example of what an estimated P&L statement looks like:

(You can download a template of this Estimated P&L statement here.)

First, add up all the earnings of the month and then the expenses incurred. Then, simply subtract the expenses from the earnings to see whether your business is making a profit (a positive number) or a loss (a negative number).

Keeping track of how well your business is doing through an evaluation of its P&L will help you see your company’s real progress as opposed to an incomplete figure suggested by high sales.

By understanding your true financial health, you can make more insightful budget decisions, such as where you need to cut costs or if you should increase prices to off-set low-profit margins.

Step 6: Make adjustments

Business budgets rarely stay static. Over time, you might need to adjust your budget to adapt to changing trends and their unique requirements.

For example, if your company has periods of busy business with high customer demands followed by periods of much slower business, you need to account for these highs and lows in your budget.

The trends in revenue generation should be identified for different seasons to help better forecast your future cash flow, so you can create your budget plan accordingly.

This will allow you to save enough money from the busy seasons to offset the period of slower sales and help your startup run more smoothly. It will also provide insight into how much labour and raw materials each season or spike might require, which can then be adjusted in the budget plan.

Other external factors like changing economic or industry trends may also demand budget adjustments.

You also need to be well-educated regarding the trends in the industry your business operates in and read up on the opinions of credible industry experts. This circles back to the importance of market research, which you should conduct thoroughly before spending any money on your business.

Market research should also be conducted and evaluated often. For example, ongoing market research will keep you apprised of any potential unfavourable economic conditions in the future, thus giving you ample time to start saving up or researching ways you can cut costs in your budget.

Of course, you may also face unexpected and unpredictable events as well, which is where your emergency fund comes in handy (more details in the next section).

Further, if your industry is expected to develop newer processes or use the latest technology, you can plan ahead for the necessary expenses your business will need to incur to keep in pace with the industry standards.

By predicting these changes and accounting for them in your budget, you’re more likely to avoid major financial problems and maintain a healthy financial outcome.

Step 7: Set up an emergency fund

When running your own business, some expenses will sneak up on you when you least expect them. These may come in the form of sudden repairs required for your equipment or an unexpected increase in your monthly rent.

You may also come across customers who are unreliable with their payments or pay invoices late, which can throw your budgeting off considerably and have drastic effects on your cash flow.

Rather than be taken in by surprise by these unpredictable financial demands or scenarios, make room for any unforeseen expenses via an emergency fund.

This fund serves primarily to support you in times of need. While the amount that you should stockpile in your emergency fund will vary based on your business type, best-practice is to put aside enough money to cover three to six months of expenses need be.

This should give you a healthy cushion to build up enough revenue to operate without needing to continue dipping into your emergency fund or to figure out how to cut costs to offset any newfound expenses.

Keeping this money separate from your day to day business funds will mean you know exactly how much you have set aside for an emergency, and you can even earn interest on it with a dedicated business savings account.

Step 8: Plan regular budget reviews

It’s not enough to simply build a budget plan and refer to it every now and again. Your budget plan must be actively revisited and re-evaluated, preferably each time you deal with major expenses.

This will help you to keep a pulse on your financial health and subsequently stop you from spending money you can’t afford to spare.

When reviewing your business budget, there are two main areas you need to pay attention to: revenue and expenses.

At the end of each month, you should draw comparisons between the revenue projection stated in your budget plan and the actual income of your business. If there are any major shortfalls or unexpectedly high turnovers, you should analyse whether this was a result of unrealistic targets or whether the business faced external difficulties.

Similarly, you should review your actual expenses against your budgeted ones and try to identify where the costs differed from your budget plan.

You can use a simple expenses spreadsheet to keep track of your monthly expenses:

(You can download a template of this Expenses Spreadsheet here.)

With these insights in hand, adjust your budget accordingly to account for any differences detected. Entering relevant numbers and readjusting as changes occur will ensure your budget is as accurate and reliable as possible to guide you in the moments you consult it.

💡 Expert Insights

As Tide’s Cash Flow Expert and, with over 40 years experience of credit management, Philip King is passionate about cash flow and supporting small businesses.

Previous roles he has held include that of Interim Small Business Commissioner for the UK Government during 2020 and 2021. This involved providing support and advice to small businesses on their trading relationship with customers, particularly in respect of payment issues. As the Chief Executive of the Chartered Institute of Credit Management between 2005 and 2020, he also promoted the importance of effective cash flow management across industry by working with small businesses to improve their payment performance.

Q1: Do I need to have a cash flow plan as well as a budget?

Yes definitely. A budget is primarily designed to make sure the business has enough sales volume, is making enough profit, and is heading in the right direction. A cash flow forecast allows you to plan that you have sufficient money in the bank to meet bills as they fall due. Putting it simply, a budget is about the progress of the business and looks at performance against plans; the cash flow forecast is more focused on timing of receipts and expenses, and concentrates on the bank balance.

Businesses fail when they run out of cash, so monitoring cash flow is crucial. Businesses that monitor their progress against a dynamic budget, and keep a close eye on cash through a regularly updated cash flow forecast are more likely to succeed and flourish.

Q2: How do I manage invoices not being paid on time?

The work to make sure your customers pay, you should start before receiving their first order. For more information on how you can maximise your chances of being paid promptly, look at the Tide resources focusing on this through a series of five questions: Why, Who, When, How, Where.

If the amount of money involved is significant, then talk to the customer before the due date to make sure the invoice has been received, approved, and is scheduled for payment. Otherwise, chase payment immediately after the due date is reached. Never sit and do nothing.

If you find out that the invoice is going to be paid late, reflect the new date in your cash flow forecast so you can see the likely impact on your bank balance. This will tell you if you’re going to need to dip into your emergency fund, or whether you need to look to raise funds from another source to fill the short-term gap.

Q3: How often should I review my cash flow plan, and why?

Every day if possible, but never less than weekly.

Your cash flow forecast should tell you how much is being received in, and paid out, on each day. If money you’re expecting doesn’t arrive and your expenses occur as planned, a hole can open up and your bank balance can become negative. If you have no overdraft arranged, emergency fund, or alternative source of finance, you could be in real trouble. Remember that businesses fail when they run out of cash.

Checking daily means you’ll know immediately if an invoice hasn’t been paid be able to chase payment. It’s vital to do that. Regular monitoring will allow you to keep your finger on the pulse and, if necessary, delay expenses to ensure the bank balance remains positive.

Cash is the lifeblood of business and you need to always be on top of it.

Wrapping up

An effective business budget takes considerable time and effort, but it is worth every moment you put into crafting it.

With a dependable business budget in hand, you’ll be more likely to make insightful spending decisions. It will also serve as a barrier that helps you to steer clear of risky expenses and objectively analyse every business expense you make.

If budgeting feels out of your wheelhouse or too time-consuming to manage alone, you can hire an accountant to help you craft one. Alternatively, you can use our free startup budget spreadsheet to help you get started today.

Photo by mentatdgt, published on Pexels