How to avoid and rectify common VAT mistakes

From reclaiming VAT on business purchases to improving your professional image, being VAT registered offers many benefits to small businesses. However, reaping the rewards whilst staying VAT compliant relies on you completing accurate VAT returns— a task that isn’t always straightforward.

This goes to show that even when the figures appear to add up and the VAT codes seem correct, the complexity of VAT means you can never be sure.

By knowing where mistakes often take place you can easily avoid making them yourself. This will help your efforts massively.

In this post, we’re going to take you through the most common VAT return errors to help you complete your returns accurately and show you what to do if you end up making a mistake.

Table of contents

- 9 common VAT return mistakes made by small businesses

- How to correct common VAT errors

- How to avoid VAT mistakes

- Wrapping up

9 common VAT return mistakes small businesses make

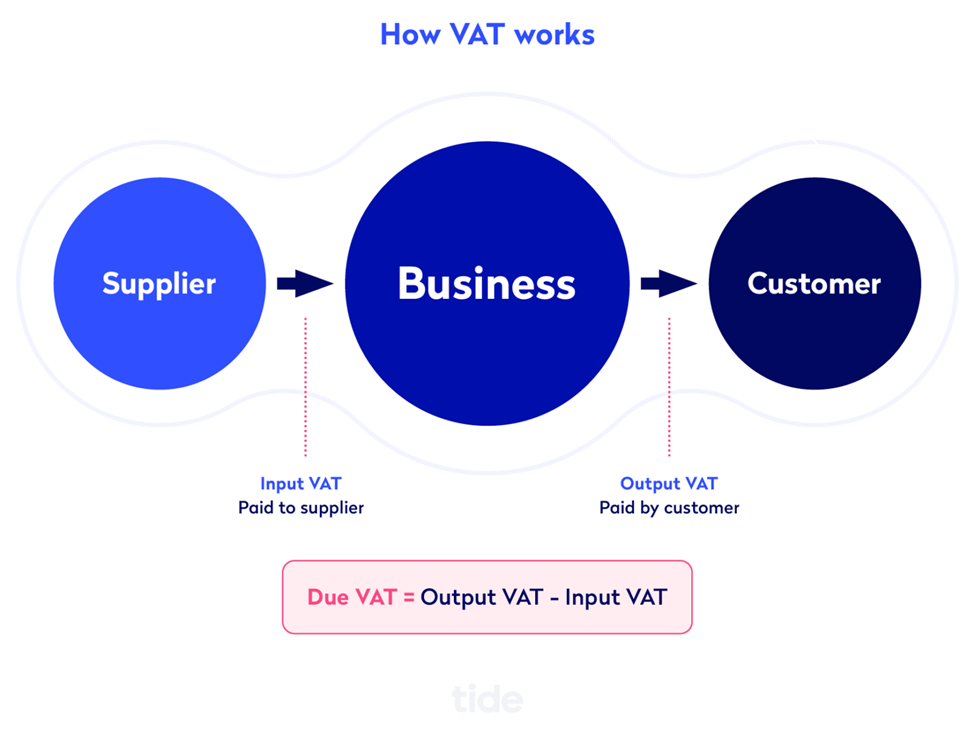

VAT, or value-added tax, is relatively straightforward in theory. It is a tax imposed by the government that is collected by VAT registered businesses at every stage in the production line.

Where VAT becomes more complicated is when it comes time to file your VAT return. You are responsible for telling the government exactly how much VAT you charged to customers (known as output tax) as well as how much VAT you were charged by suppliers (known as input tax).

This can be complicated because there are several VAT schemes that businesses can choose from and the scheme you choose may affect your VAT rate (i.e. how much VAT you charge to customers).

Your chosen VAT scheme also affects how to report that VAT on your VAT return (namely whether to report gross or net income) as well as how often you can reclaim your input tax. We’ll explain the various VAT schemes in more detail in a later section.

Further, there are several goods and services that are either VAT exempt (or qualify for partial exemption), out of the scope of VAT entirely, or charged at a reduced-rate or zero-rate. You alone are responsible for figuring out if you sell any items that fall into these categories, what amount of VAT to charge if you do and exactly how to report those special cases.

If you’re confused, you’re not alone. Understanding the 9 most common VAT return mistakes that small businesses make, as well as how to avoid them, will put you in a much better position to avoid making them yourself.

Top Tip: Before you continue, it’s important that you understand the fundamentals of VAT, which you can learn about in our guide to everything you need to know about VAT 🔎

1. Entering the wrong figures

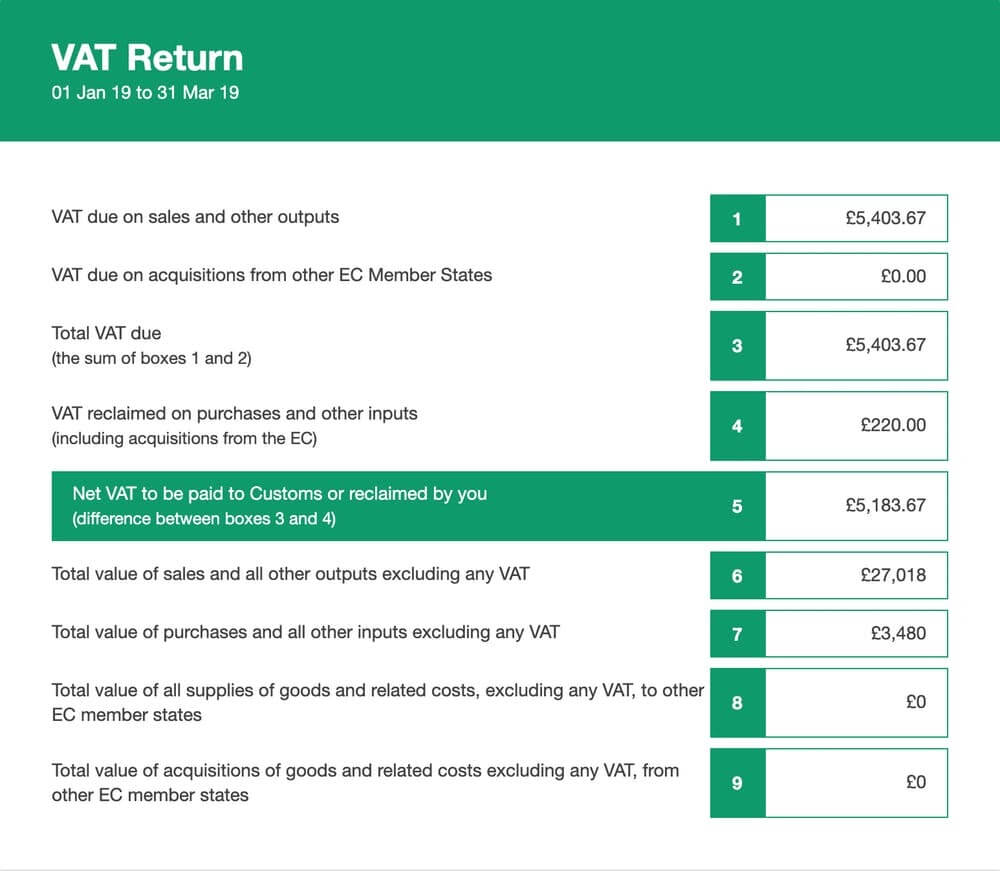

Most of the mistakes when it comes to entering accurate figures arise with box 6 on the VAT return form, which represents the ‘total value of sales and all other outputs excluding any VAT’.

This is because the amount that needs to be entered into box 6 depends on which VAT scheme you’re using.

If you’re using the flat rate VAT scheme, the amount entered into box 6 should be the gross income you’ve applied the flat VAT percentage to. If you’re using the cash accounting scheme or the standard accounting scheme, box 6 should include your income net of VAT.

For example, let’s say you’re using the flat rate scheme with a flat rate percentage of 14.5% and a quarterly VAT inclusive income of £30,000. Your box 6 figure will be £30,000 and your box 1 figure for ‘VAT due on sales and other outputs’ will be £4,350 (14.5% x £30,000).

If you’re using cash or standard VAT accounting, box 6 will be your income net of VAT, so £25,000. Box 1 would then show £5,000.

It’s important to double-check that the figures entered into box 6 and box 1 are correct in relation to the accounting scheme you’re using.

2. Reclaiming VAT on fuel and cars

VAT on fuel purchased by business directors, partners and employees for business purposes can be reclaimed on a VAT return.

A common VAT return mistake is when fuel purchased for personal use is claimed alongside fuel purchased for business travel, which often happens when a vehicle has dual business and personal use. HMRC expects to see detailed mileage records to support a claim, unless records are too difficult to maintain, in which case you’re able to pay a scale charge as output tax to account for fuel you’ve used for personal travel.

Similarly, HMRC doesn’t allow VAT to be recovered on the purchase of a car unless you can prove that it will be used exclusively for business reasons. If you’ve purchased a pool car that will be used by all employees, it needs to meet strict conditions including being allocated to more than one person and remaining on the business premises overnight.

Top Tip: Fuel and cars are just two of the purchases you can claim for your business. Find out what else you may be entitled to in our guide to reimbursable expenses and how you can claim them 🚗

In addition to the purchase of a car, mistakes are commonly made on lease cars, where 100% of VAT is recovered as input tax. Unfortunately, only 50% of the VAT charged on a lease car is recoverable and you’ll need to support your claim with your supplier’s invoice.

3. Not charging VAT on non-standard supplies

Charging VAT on core business supplies such as stock and office supplies is a regular occurrence. Because these purchases are included in every VAT return, mistakes rarely happen. Where errors creep is when non-standard supplies are added.

Transactions outside of regular trading patterns such as cash sales, property income, management charges or barter transactions can often be overlooked or given the wrong treatment, resulting in too little, too much or no VAT being reclaimed.

Make sure to highlight every new or unusual transaction so that you can be sure that it’s given the correct treatment.

4. Reclaiming VAT on entertainment

Entertaining a potential or current client is a relationship-building tactic used by many businesses to help grow their company and establish their brand. Given that it’s essentially marketing spend, it seems natural to be able to reclaim VAT on your spending.

Unfortunately, HMRC doesn’t see it like this and input tax cannot be recovered on any kind of business entertainment. This includes:

- Food and drink

- Accommodation

- Entry to events or shows

5. Reclaiming VAT on deposits

Another common mistake made by businesses is recovering VAT on deposits instead of waiting until the full balance has been received.

Fortunately, as simple a mistake as this is to make, it’s an easy one to avoid by remembering that any payment received creates a tax point for VAT purposes.

So, if your business takes a deposit or down payment from customers for goods or services, VAT is due when that initial payment is received, unless you have already issued an invoice.

Top Tip: If you’re a VAT registered company, you’ll need to provide and record VAT invoices. Get up to speed on what information you must include on your VAT invoice 💡

6. Reclaiming VAT on aged creditors

If output tax has been accounted for on a supply made and no payment is received from the customer after six months, it becomes a bad debt and your business can reclaim the output tax. This is a commonly known debt relief rule.

But the rule has another side that often goes overlooked: you can’t claim bad debt relief until after six months from the due date.

If your business has recovered input tax on invoices received from suppliers, but the payment to the supplier remains outstanding after six months, you’re required to repay that input tax to HMRC.

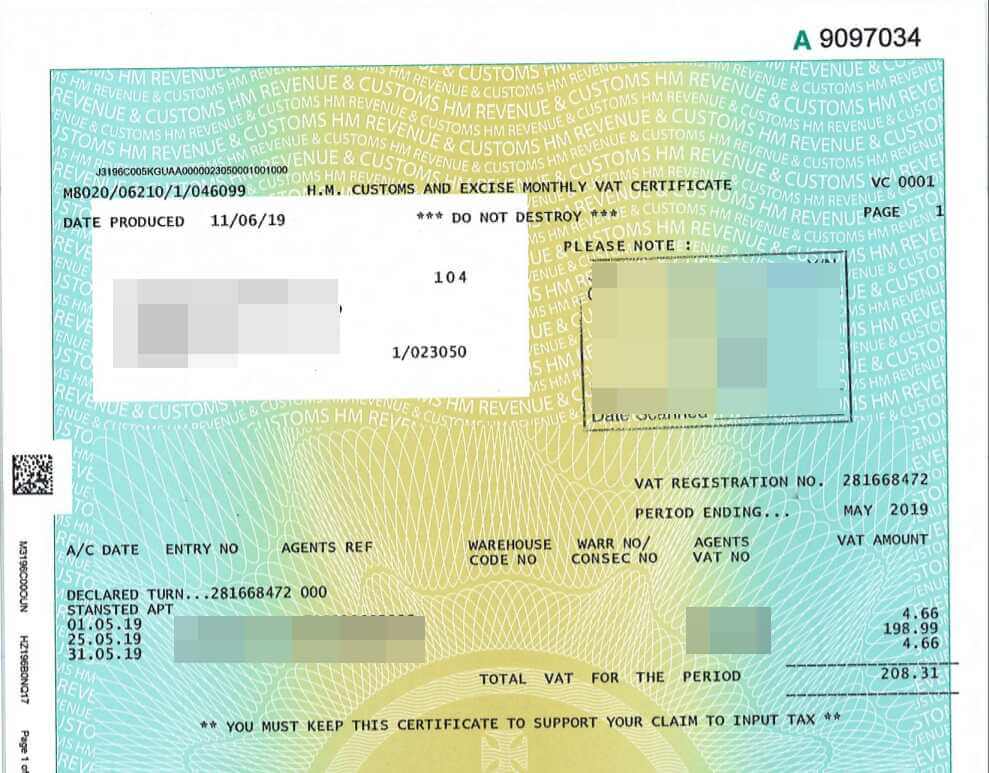

7. Reclaiming import VAT too early

The most common mistake made with import VAT is reclaiming VAT on receipt of invoices from shipping agents. While these invoices are valid, where claims are concerned they only account for the agent’s charges and not the import VAT.

You can only reclaim import VAT on receipt of an official import VAT certificate (C79) from HMRC. This is usually received around three weeks after the end of the month you received the goods in the UK.

Hold off on any claim until the C79 certificate proves you are the owner of the goods.

Top Tip: If your business exports goods and services, it’s important you learn how export VAT is charged in the EU and the rest of the world. Check out our guide to VAT rules and rates on exports 🚢

8. Reclaiming VAT without invoices

To reclaim VAT on any business expense, you must provide evidence in the form of a VAT invoice. Therefore, it’s important that you get all paperwork in order and chase up any missing or late invoices before submitting your tax return.

If you’ve misplaced a VAT invoice and can’t obtain a copy of it, HMRC may accept alternative evidence such as a bank statement showing that the payment was made to a supplier. However, the general rule of thumb is no evidence = no claim.

9. Claiming on zero-rated and partially VAT exempt purchases

Given that many of the major and common purchases you make for your business include the standard rate of VAT (20%), it’s easy to assume that VAT can be recovered on every business expense. However, this isn’t always the case.

Some purchases, such as the selling, leasing and letting of commercial land and buildings and subscriptions to membership organisations, are VAT exempt and therefore cannot be added to a VAT return. Other items have a reduced-rate (5%) or a zero rate of VAT but are still considered taxable and therefore must be included in your VAT returns.

Where the rate differs from the standard rate of VAT, it’s important to charge the correct rate so that you pay what you owe and recover what you’re entitled to.

Personal expenses are exempt too, although you may be able to claim a proportion of the VAT back on an item that has dual business and personal use. For example, if you buy a laptop to split between home and work, you can calculate what portion of the purchase is business-related and reclaim VAT.

You can find a full list of UK VAT rates on different goods and services on the GOV.UK website.

How to correct common VAT mistakes

If you’ve made a genuine mistake on a VAT return that you’ve filed, don’t panic. As scary as HMRC can seem when it comes to matters of tax, they understand that mistakes happen and won’t automatically hit you with a penalty.

In most cases, providing the error meets HMRC’s conditions, you don’t need to report it. You can simply correct it by making adjustments on your next VAT return.

HMRC’s VAT return adjustment conditions

You can correct errors on any VAT return that relates to an accounting period that ended within the last four years if they:

- Are below the net error reporting threshold of £10,000. Errors of more than £10,000, up to a maximum of £50,000 can also be adjusted if the error is not more than 1% of the figure entered in box 6. Errors that exceed the threshold must be reported and cannot be adjusted on a future VAT return.

- Are not made on purpose (i.e. not a ‘deliberate error’).

Making an adjustment on your VAT return

Making an adjustment is a straightforward process that you can do in one of two ways:

- Adding the net value to box 1 (‘VAT due on sales and other outputs’) for tax you owe.

- Adding the net value to box 4 (‘VAT to be reclaimed on purchases and other inputs’) for tax due to you.

For example, let’s say a small business owner called Rachel is VAT registered under the standard VAT scheme and submits VAT returns every quarter. When preparing her year-end accounts in December, she noticed that she recorded the same purchase invoice for £1,500 plus VAT (20%) twice: once in February and once in March.

This means that she over-claimed VAT in the amount of £300 in the VAT period ending March 31st. Because it was a genuine mistake made within the reporting threshold and within the last four years, she can correct it on her next VAT return by adjusting the figure in box 1. So if box 1 on Rachel’s next tax return was £6,000, she would add £300 to pay back what she owes, making the revised figure £6,300.

When making an adjustment, HMRC also asks that you:

- Keep details of the error (e.g. how it happened, the date it was discovered and the amount of VAT involved)

- Include the value of the error in your VAT account

Reporting an error on your VAT return

If your error does not meet the adjustment conditions, you need to report it to HMRC by completing form VAT652 and sending it to the VAT Error Correction Team. You’ll then be notified of whether the amount you calculated is correct and how much interest or tax you owe.

If the error was made as a result of dishonest or careless behaviour, HMRC can charge you a penalty of up to:

- 100% of any tax under-stated or over-claimed if you send a return that contains a careless or deliberate inaccuracy.

- 30% of an assessment if HMRC sends you one that’s too low and you do not tell them it’s wrong within 30 days.

- £400 if you submit a paper VAT return, unless HMRC has told you you’re exempt from submitting your return online.

You can find further information on correcting VAT return errors and penalties on the GOV.UK website.

How to avoid VAT mistakes

While there’s no sure-fire way of preventing mistakes, you can reduce your chances of needing to make an adjustment by understanding VAT and having a system in place that makes filing returns as stress-free as possible.

1. Understand VAT schemes

By understanding the three main VAT schemes for small businesses, you’ll be able to choose the one that’s right for your business and ensure the figures on your VAT return are correct.

We briefly mentioned these above, but here are the three main VAT accounting schemes in more detail:

- Flat rate VAT scheme. You charge clients or customers at the standard rate of VAT (currently 20%) but pay a reduced percentage to HMRC. By benefiting from this favourable rate, you’re unable to claim VAT on expenses other than capital equipment.

- Cash accounting VAT scheme. You only pay and reclaim VAT on the money you’ve paid and received.

- Standard accounting VAT scheme. You pay VAT on sales regardless of whether you’ve been paid by the client or customer. You then reclaim VAT on supplier invoices, regardless of whether you’ve paid the bill.

The VAT schemes that you are eligible for upon VAT registration depends on your taxable turnover and affects how often you can reclaim VAT. This table explains each scheme in more detail.

Top Tip: You have to register for VAT when you reach the VAT threshold. Before that, businesses can choose to voluntarily register, though there are pros and cons to that decision. To learn more about the VAT threshold in the UK, read our guide to the VAT threshold and when should you register for VAT 💫

| Turnover | Client type | VAT options | Benefits | Drawbacks |

| Less than £85,000 | Mostly non-VAT registered customers | Don’t register for VAT | Don’t need to pay or charge VAT | None |

| Less than £85,000 | Mostly VAT registered customers | Voluntarily register for Standard Rate VAT | -Reclaim VAT you’ve been charged -Reclaim throughout the year -Look more established | -More paperwork -Your outgoing invoices may increase to account for VAT |

| From £85,000 to £150,000 | Any | Register for Standard Rate VAT or Flat Rate VAT | If Flat Rate: -Don’t have to pay VAT on every purchase -Simplified record-keeping which saves time | If Flat Rate: -The VAT % varies greatly by sector |

| Less than £1.35 million | Any | Register for Standard Rate VAT, Flat Rate VAT, Cash accounting scheme or Annual accounting scheme | If Cash accounting scheme: -Don’t pay or reclaim VAT until actual money changes hands for purchases and sales -Improves cash flow as you only pay VAT once you are paid If Annual accounting scheme: | If Cash accounting scheme:-Lots of paperwork -If customers pay invoices on time, this scheme won’t make much of a difference on cash flow If Annual accounting scheme: |

2. Keep accurate records

A number of the VAT mistakes we’ve covered in this post come from poorly maintained records. The risk of listing net figures as gross, reclaiming VAT too early on imports, reclaiming VAT without purchase invoices and recovering VAT too early from creditors can all be reduced with good bookkeeping and accurate records.

Here are some tips for better record-keeping:

- Label trading records by document (e.g. invoices and receipts) so that you can easily pinpoint figures.

- Create a folder that contains copies of your VAT certificate, submitted VAT returns and all correspondence with HMRC.

- Monitor your VAT account in an accounting system.

- Keep copies of all VAT invoices and self-billing agreements (invoices prepared by the customer on your behalf).

- Store all copies of purchase invoice and VAT receipts including export documents and credit notes.

- Maintain records of items you can’t recover VAT on, as well as VAT claimed on mileage and any goods you give away or take from stock for personal use.

Although the cut off date for adjustments is four years, you must keep VAT records for six years after the date of your VAT return.

If you lose paperwork or it gets damaged, ask the supplier to provide a duplicate.

Top Tip: Good bookkeeping helps you keep tabs on your day-to-day financial data, monitor your cash flow and evaluate your success. To improve your own, take a look at our beginner’s guide to bookkeeping 📖

3. Put someone in charge of VAT

Placing someone in charge of dealing with VAT day-to-day will help to avoid any confusion around tax and ensure records are consistent. If you’re confident about VAT and the various regulations, you can take on this role yourself using accounting software to file quarterly returns directly from your Tide account.

If not, delegate the role to someone with sufficient knowledge and expertise to keep you VAT compliant. The most obvious choice being an accountant.

Top Tip: If you don’t already have an accountant and aren’t sure how to find the right one for your business, read our guide to choosing an accountant for your small business 📒

4. Use MTDfV compatible accounting software

MTDfV stands for Making Tax Digital for VAT — a program introduced by the government to make submitting VAT returns easier by helping businesses store records digitally to automate payments and returns. MTDfV-compatible software, like Tide Accounting, lets you submit VAT returns without the need to visit the HMRC website.

Top Tip: Making Tax Digital is designed to reduce the risk of human error in VAT and tax returns. To find out more about how it works, check out our guide on what Making Tax Digital means for your small business 💻

5. Keep up to date with HMRC changes

VAT is constantly evolving. Both the flat rate scheme and Making Tax Digital are recent changes that have transformed VAT treatment for small businesses. With the ongoing situation around COVID-19 and Britain’s withdrawal from the EU (Brexit), as well as HMRC’s drive towards making VAT easier for VAT-registered companies, there’s likely to be new rules and regulations to come.

Stay abreast of any developments through reputable sources like the GOV.UK website, news websites and blogs like this one to ensure you don’t fall foul of VAT errors.

Wrapping up

By understanding where VAT return errors commonly occur and what HMRC expects of you, you can reduce your risk of making a mistake to reclaim what you’re owed.

That said, none of us are perfect. Despite our best efforts, mistakes can happen. If you realise you’ve entered the wrong figures on your VAT return, try not to stress. You have up to four years to put things right.

By keeping your finances in order and all VAT related paperwork organised, mistakes can easily be rectified on future returns.

Photo by Kate Oseen, published on Unsplash